Surging Property Insurance Costs: Implications on Commercial Real Estate

The commercial property insurance market has seen accelerating increases in premiums since 2017 and some of the fastest growth rates in recent history. These increases have direct implications for commercial real estate investors, impacting tenants, cash flow, valuations, and the ability to secure debt financing. Whether you are an experienced investor with a large portfolio, a mom-and-pop investor with one or two assets, or a 1031 exchange buyer trading into a new market, the impacts of insurance on property performance cannot be overlooked.

Factors contributing to the rise of property insurance in commercial premiums include:

- Increased frequency and severity of natural disasters.

- Secondary perils are on the rise (i.e. an earthquake causes a fire).

- Rising claims and larger investment losses.

- Reinsurance capacity and pricing.

- Inflation / persistent construction cost and wage increases.

- Property valuation challenges against a difficult economic backdrop.

- Regulatory changes – keep an eye on building performance standards.

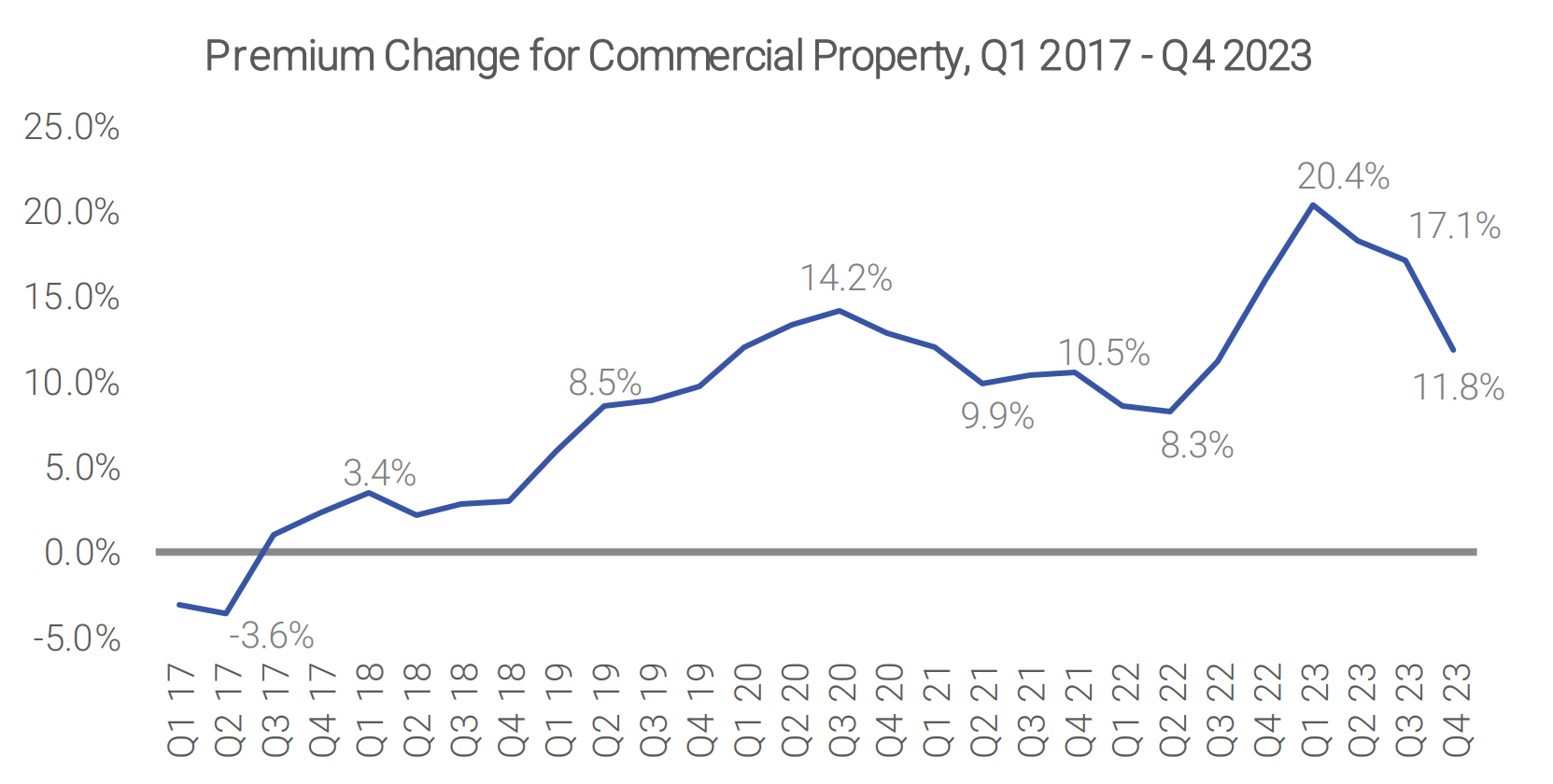

Commercial property budgets can no longer assume insurance premiums will increase at nominal rates over the prior year, nor can investors assume they will be able to achieve the same rates as the previous owner. While the acceleration of rate increases slowed in Q4 2023 commercial property insurance still outpaced all other insurance lines at 11.8%. According to industry experts’, premiums are expected to increase between 5% – 25% over the coming year. Regions exposed to CAT events (“catastrophic event property deductible”) will see a sizably larger increase in premiums ranging from 15% – 25% vs. CAT-free regions which are anticipated to see increases in the 5% – 15% range.

Source: Council of Insurance Agents & Brokers

Cause for these continued increases can be seen nationally in 28 separate events in 2023 resulting in billion-dollar disasters.

Source: National Oceanic and Atmospheric Administration

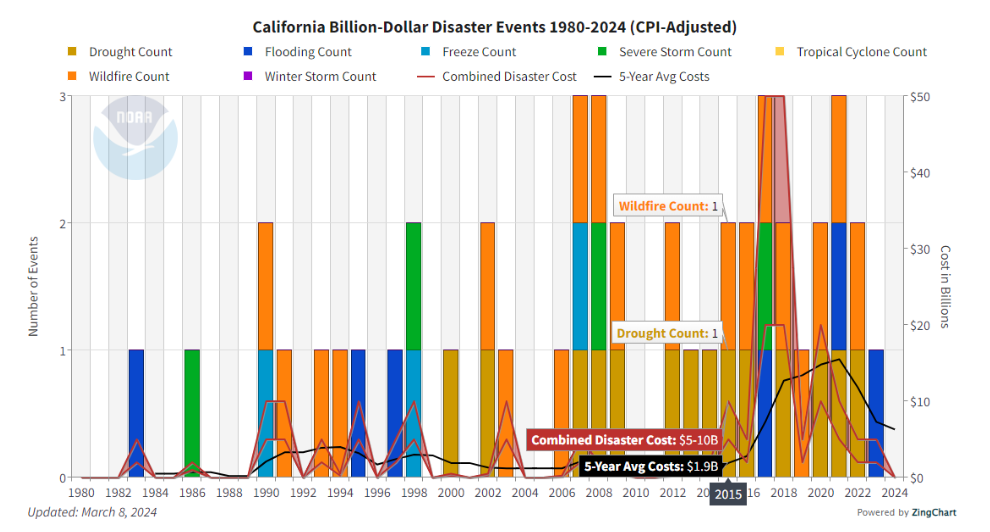

For California investors, drought, wildfires, and flooding have had the largest impact on insurance premiums for commercial properties, with significant increases in frequency and financial impact over the past 10 years. The impact for properties in low-lying areas or dense foliage should be considered fully and assessed against similar investment opportunities not exposed to these hazards.

Source: National Centers for Environmental Information

Considerations for property owners & developers

- Property Valuation: Depending on lease structure an increase to insurance costs may result in a direct hit to property net operating income (“NOI”). For example, a $10,000 increase to a property’s insurance premium that an owner is unable to pass through to the tenant would result in a decrease in value of approximately $143,000 at a 7% cap rate.

- Tenant relationship:

- A tenant’s ability to absorb an increase to commercial insurance costs with their property will differ greatly. A small mom-and-pop store or startup business may be crushed with the additional cost of insurance if passed through, while a corporate entity is likely better equipped to absorb the increase. At the same time, the corporate entity will also be more prepared to renegotiate their lease at their first opportunity to mitigate the impact to their own NOI.

- As operating costs passed through to tenants increases the demand for space in the subject property may become less desirable compared to competing properties. If demand for a particular property drops due to increased operating costs, rents will need to be adjusted downward to maintain occupancy, resulting in lower NOI and property valuation.

- Lender Requirements: Three factors to consider that may limit or eliminate an investor’s ability to obtain debt financing:

- Property location and exposures to hazards may affect borrower’s ability to secure insurance that complies with lender loan requirements.

- Property cash flow and possible DSCR triggers if the required insurance causes a surge in premium pricing.

- Increased hazards in certain markets are causing lenders to pull out all together, limiting borrower options and increasing the cost to borrow money.

- Portfolio Exposure: Owners may be over concentrated in a single market with a high likelihood of a devastating hazard and may need to consider exchanging into new markets and/or property types to mitigate long-term risks.

- 1031 Exchange: Buyers in a 1031 exchange who are looking to simplify their portfolio by investing in more passive single-tenant assets with NNN lease structures need to understand who their tenant is under the lease. For example, if you are in an exchange and comparing NNN purchase options, you should consider if your lease is with a corporate entity or a franchisee, the former being much more likely to absorb increases in operating costs. Many developers who crank out numerous NNN properties annually that are sold to 1031 exchange buyers can achieve lower premiums through blanket policies. A new purchaser may be hit with a sizable increase, which if not communicated to the tenant properly may be a shock to their business operations and start the new owner off on a bad foot with their tenant.

- Development Challenges: New projects are facing increased costs and regulatory challenges, which will be further exasperated by building performance standard (i.e. restrictions on building emissions). Properly budgeting for increased costs will be key to securing the best debt financing.

- Buyer preferences: Decreases to NOI and the increased risk of loss due to hazards may shift buyer purchase preferences. As buyer preferences shift away from certain markets cap rates will likely increase and result in lower property valuations and shrinking buyer pools.

Tips for commercial property owners

- Identify hazard exposure and take the necessary precautions to protect your property (i.e. installing fire resistant roofs, storm shutters, etc.).

- Implement risk mitigation measures specific to buildings and tenants.

- Implement strong property management practices. Address property issues immediately to reduce / eliminate insurance claims.

- Document and share your risk mitigation measures with your insurance broker and the underwriter.

- Begin the renewal process early. According to the Council for Insurance Agents and Brokers in Q4 2023 sixty-four percent (64%) of surveyed respondents reported a decrease in underwriting capacity. Don’t wait until the last minute to update your policy, start early, and provide yourself ample time to find the best solutions to your property needs.

- Address recommendations by your insurance broker / carrier.

- Work closely with your insurance broker to update your insurance-to-value calculations and monitor commercial property limits to avoid underinsurance and coinsurance penalties.

- If selling, communicate openly with purchasers on your insurance costs and any risk mitigation measures put in place to reduce costs.

- To best mitigate the impact of rising insurance costs, stay informed and continually assess and reassess steps that can be taken to reduce property exposures and the impact to your bottom line.

CapWise Commercial Advisors, Inc. (“CapWise”) is here to help property owners assess the impact of their commercial property insurance on their asset and portfolio performance. From updating valuations, assisting with due diligence on an acquisition or 1031 exchange, to securing debt financing, we are in your corner and your advocate in the marketplace. Please call or email to learn how CapWise can help.